The first half of 2024 saw muted transaction activity as financing costs kept potential buyers sidelined. However, we may start to see signs of recovery in the second half, especially as new construction slows and demand for space remains robust across key property sectors. Multifamily and industrial demand has leveled off at sustainable levels, while retail has emerged as an unexpected performer, with decreasing vacancy rates and positive net absorption in recent quarters.

Supply and Demand Dynamics

Despite the uptick in vacancy rates across most sectors due to new

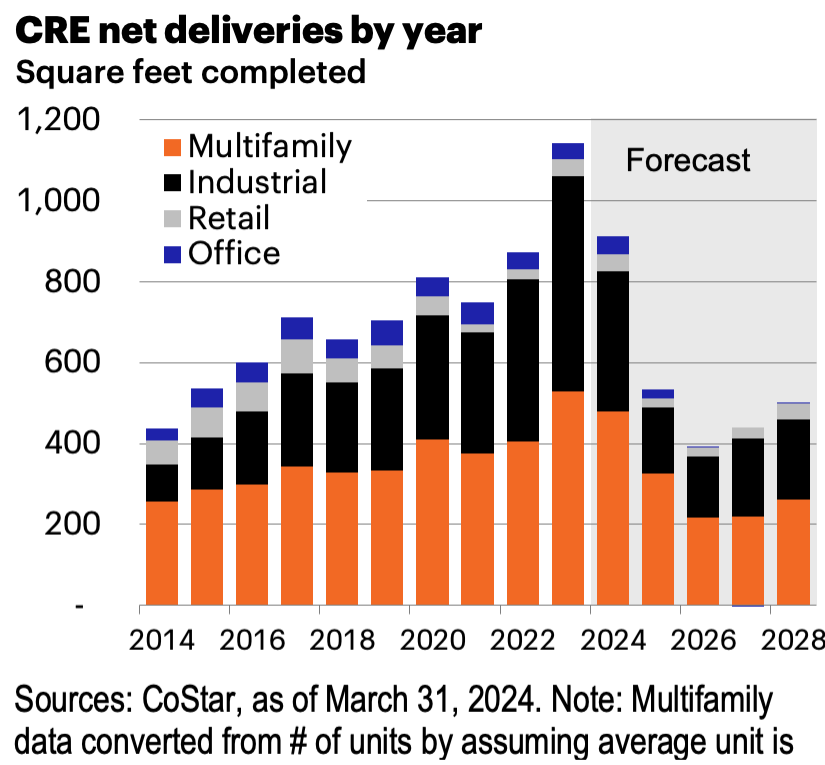

completions, demand for commercial space remains solid. Over the past year, the U.S. delivered 612,000 new multifamily units and 515 million square feet of industrial space, reflecting a significant increase in supply. However, this wave of new supply may be short-lived, as construction activity is already declining sharply, with both multifamily and industrial groundbreakings falling to levels last seen in the early 2010s.

The decline in new construction is largely attributed to rising financing costs, which have made it more difficult for developers to break ground on new projects. This decline in construction is expected to lead to a supply gap in the coming years, especially in sectors like multifamily and industrial, where demand remains strong. As a result, we anticipate that vacancy rates will fall and rent growth will reaccelerate over the medium term.